Stable Market • Solid Inventory • Some Segmentation

The Park City real estate market and the greater Wasatch Back continued to show impressive resilience through the third quarter of 2025, with steady, reliable growth across most property segments. Despite evolving national trends, our local market remains driven by lifestyle demand, strong buyer confidence, and continued interest in year-round mountain living.

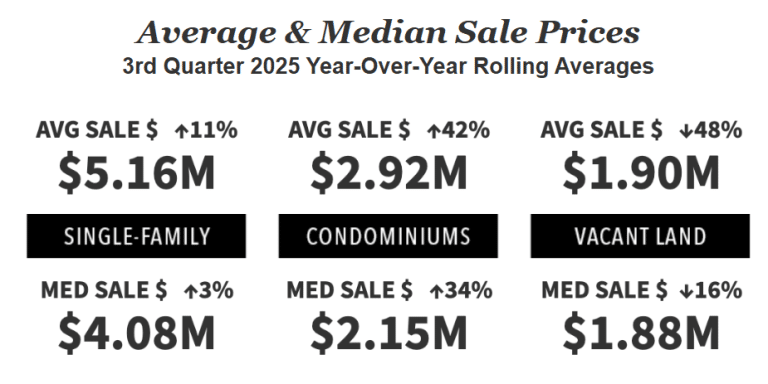

Across Summit and Wasatch Counties—our primary market area—closed sales were up 6%, reaching 2,678 transactions, while overall sales volume increased an impressive 25%, surpassing $5.5 billion. Buyers are clearly still choosing Park City not only as a resort destination, but as a long-term investment and lifestyle home base.

Market Performance & Inventory Trends

Single-family homes showed consistent strength across all areas, while condominium and vacant land sales varied depending on the neighborhood. Distinctions also emerged between newer and older properties, as well as across price points, which we explore in greater detail below.

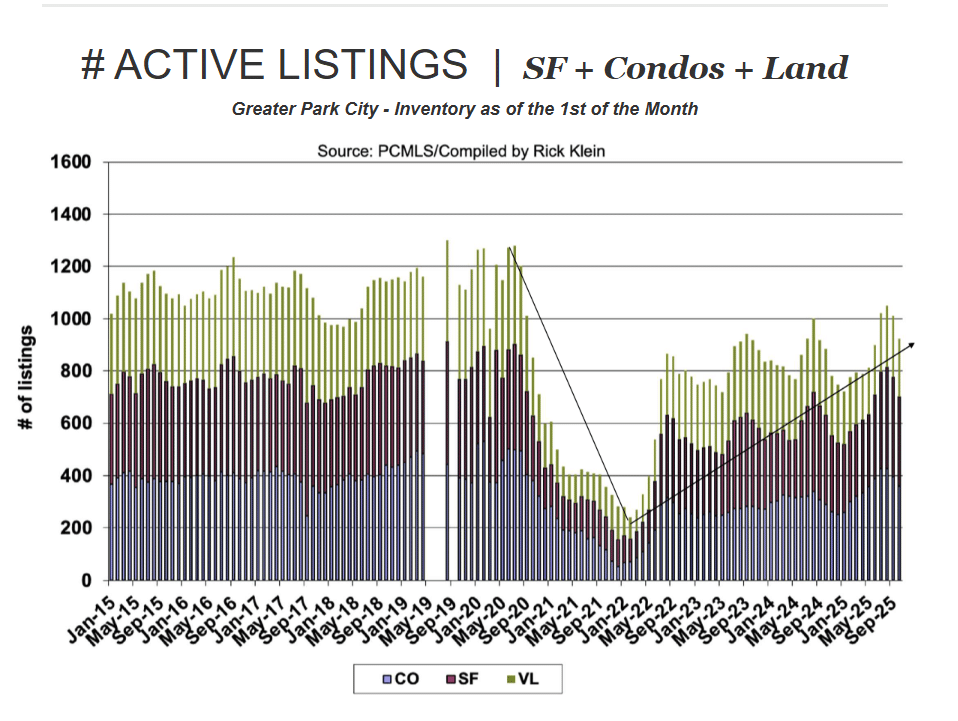

One of the most notable shifts this quarter was the rise in inventory. For the first time since 2020, active listings climbed above 1,000 units, offering more choice for buyers while preserving healthy values for sellers.

Every area—from Old Town and Park Meadows, to Deer Valley, Canyons Village, Promontory, and the Jordanelle Basin—continued to show its own unique pattern. Whether you’re following Deer Valley condos for sale, investment opportunities in Canyons Village, or primary home neighborhoods in Thaynes Canyon, Pinebrook, or Jeremy Ranch, Q3 delivered meaningful insight across all property types.

Key Market Trends shaping Q3 2025

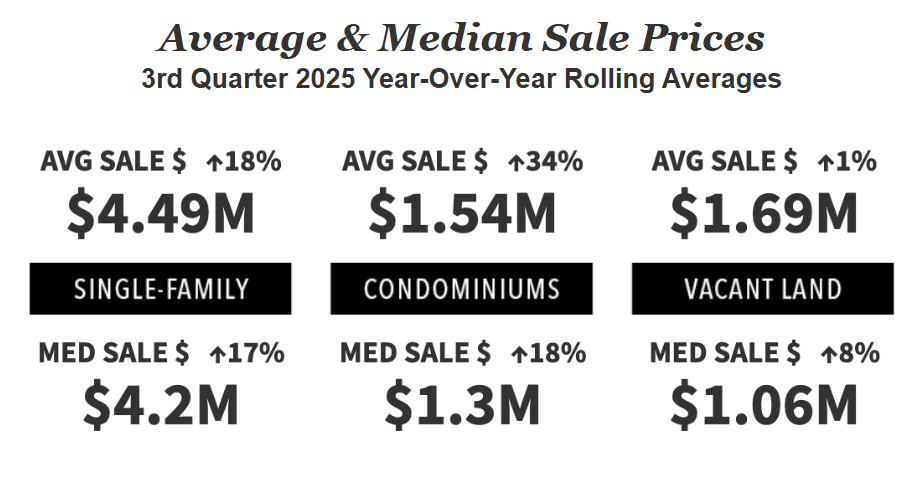

Prices & Activity I Park City Proper

High-End vs. Entry-Level: A Clear Market Split

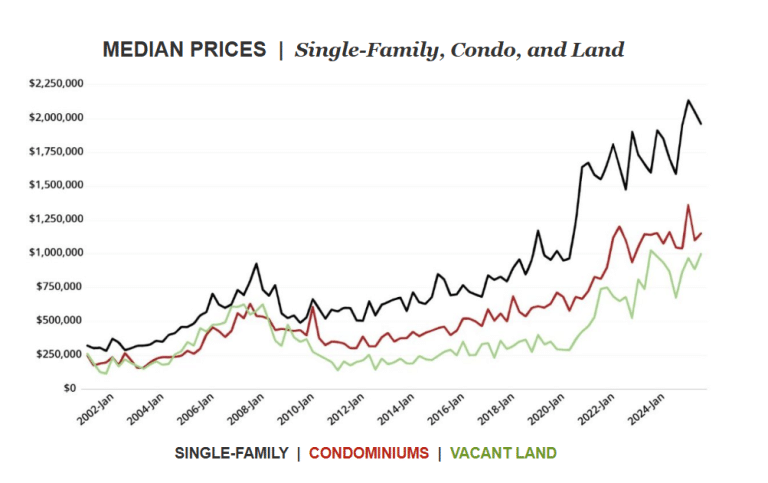

Third-quarter data revealed a clear bifurcation in the Park City real estate market. Properties priced above $2.5 million significantly outpaced those below it. Properties priced above $2.5M saw a 38% year-over-year increase in unit sales and a 50% rise in total sales volume. In contrast, properties under $2.5M experienced only modest gains – up 2% in unit sales and 4% in volume. This widening gap highlights how high-net-worth buyers continue to view Park City real estate as a stable investment, often purchasing with cash and prioritizing properties that meet their exact preferences. Indeed, cash transactions accounted for more than 60% of luxury sales. Meanwhile, buyers in lower price ranges are more reliant on financing, and higher interest rates are currently tempering activity in that segment.

New Construction vs. Existing Homes

Another notable trend in our market is the strong performance of new construction compared to existing homes. When new builds are included in the combined single-family and condominium median price calculations, the year-over-year median price rose 26%. Excluding new construction, however, the median price increase was a more modest 6.7%, consistent with the historically normal rate of appreciation in the greater Park City area. This contrast highlights the premium buyers are willing to pay for move-in-ready homes. Turnkey, up-to-date properties continue to command top dollar, as many high-net-worth buyers prefer the convenience and immediacy of new construction over the time and uncertainty of renovating older homes.

Condominium Market Challenges

A number of existing condominium communities in our area are now facing significant special assessments, some exceeding six figures, to address deferred maintenance and necessary capital improvements. In other cases, homeowners’ associations are substantially increasing monthly fees to rebuild reserves for upcoming maintenance needs. These rising costs are having a direct impact on pricing and buyer sentiment. As a result, prospective condominium buyers should take extra care to review the financial health of each HOA, including reserves and planned capital projects, before proceeding with a purchase.

Inventory on the Rise

# ACTIVE LISTINGS | SF + Condos + Land

Greater Park City - Inventory as of the 1st of the Month

As mentioned in the introduction, the big news in inventory is that during the 3rd quarter of 2025 our inventory levels crossed the 1,000-unit threshold for the first time since 2020. This was welcome news, as the increased inventory contributes to a healthy buyer/seller balance in our market. Inventory level changes year-over-year by property type in the 3rd quarter were as follows:

• Single-family inventory was unchanged

• Condominium inventory was up 24%

• Vacant land inventory was down 12%

Q2 Record Sale

1851 W Galena Ridge Way

The first completed home in the new gated community of Marcella Club at Deer Valley East Village has sold. Listed at $21 million, this nearly 8,000 sq ft residence features 6 bedrooms, 9 baths, and access to one of Park City’s most exclusive ski and golf memberships.

Listing Courtesy of BHHS Utah Properties

Park City Real Estate Market Trends by Neighborhood

PARK CITY LIMITS I Market Overview

Single-Family Homes Trends

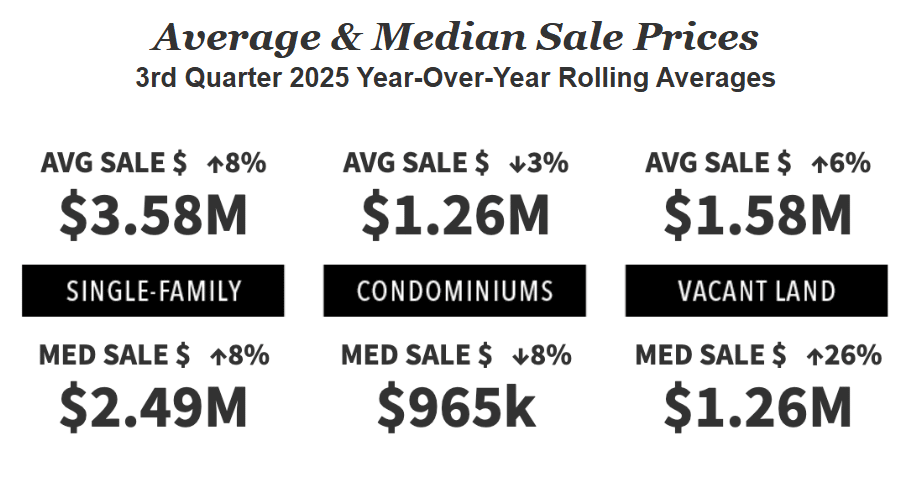

The Park City limits posted solid growth in the single-family sector this quarter, with the median home price increasing 3% to $4.0M on 137 total closings—a 23% jump in sales activity.

Here’s how key neighborhoods performed:

Old Town saw 41 home sales over the past 12 months, up 21% from the previous year, with the median price holding steady at $3.8 million.

In Thaynes Canyon, 11 homes closed, marking a 10% gain in sales and a 6% rise in median price to $4.6 million.

Lower Deer Valley experienced a 13% decline in median price to $4.1 million on 10 total sales.

Deer Crest recorded 5 closings and a 6% dip in median price to $12 million.

Upper Deer Valley also softened slightly, with 7 closings and a 4% decrease to $7.2 million.

In contrast, Empire Pass surged. Its 8 closed sales pushed the median price up 21% to $14.2 million. This was one of the strongest luxury performers, driven by ski-in/ski-out demand and Talisker membership benefits.

Aerie saw 5 closings and a notable 40% drop in median price to $4.3 million.

Prospector’s 15 total sales drove a 14% increase to $2.3 million.

Park Meadows recorded 35 closings, up 30%, with a modest 2% rise in median price to $3.5 million.

Condominiums

The overall Park City limits posted one of the strongest condominium performances in our region for the 3rd quarter. Sales were up 10% on 267 total closings, and the median price climbed a notable 34% to $2.15 million.

Deer Crest experienced a dramatic surge, driven by new inventory. Sales jumped 640% to 37 closings, with the median price up 9% to $4.4 million.

Old Town, by contrast, saw a 16% decline in sales activity with 85 closings and a 9% dip in median price to $1.1 million.

In Lower Deer Valley, sales rose 28% to 41 closings, accompanied by a 14% increase in median price to $2.5 million. Upper Deer Valley also performed exceptionally well, with sales up 16% on 22 closings and a striking 90% increase in median price to $4.8 million. Empire Pass remained steady in volume with 21 closings, though the median price rose 64% to an even $7 million. Prospector saw a slowdown, with a 28% drop in sales to 28 closings and an unchanged median price of $398K. Rounding out the area, Park Meadows posted a 19% increase in closings to 31 total sales but saw its median price fall 33% to $1.3 million

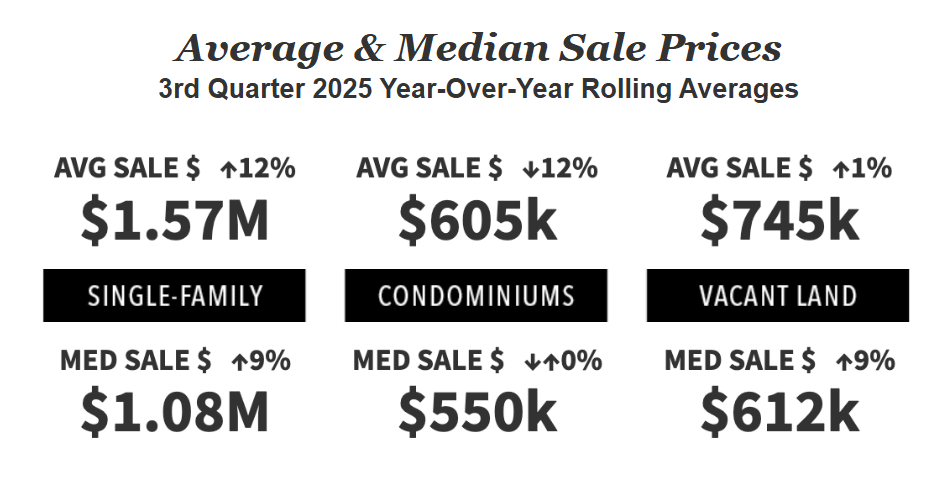

Neighborhood Highlights - Snyderville Basin

SINGLE-FAMILY Homes

The Snyderville Basin once again showed remarkable diversity across its single-family housing market, with wide variation in home types, prices, and sales pace. Over the 12-month period ending October 1, there were 362 total sales. The highest sale reached $27.8 million, with three homes selling above $20 million and twenty surpassing $10 million. On the other end of the spectrum, the lowest sale closed at $760,000, with fifteen homes under $1 million, mostly in Summit Park and Silver Creek South near I-80.

Canyons Village led the Basin in price, with a 61% jump in median value to $17.4 million on 9 total sales. Sun Peak/Bear Hollow followed closely with a 65% median price increase to $3 million across 12 closings. Silver Springs saw 26 sales with a 10% rise in median price to $2.4 million, while Old Ranch Road climbed 19% to $7.9 million on 10 transactions.

Kimball Junction was active with 13 closings and a 17% gain in median price to $1.3 million. Further east, Pinebrook recorded 28 closings with a modest 3% increase to $1.9 million, and Jeremy Ranch logged 53 closings with an 11% rise to $2.1 million. Summit Park saw 28 closed sales with a 7% median sale price decrease to $1.3 million. Glenwild posted 19 sales with a slight 4% dip in median price to $5.1 million, while nearby Silver Creek Estates saw a 13% increase to $2.8 million on the same number of closings.

Trailside Park recorded 17 closed sales with a 4% rise in median price to $1.7 million, and Silver Creek South had 27 sales with a 3% uptick to $1.2 million. Promontory remained one of the most active neighborhoods in the Basin with 101 total closings, though its median price held steady at $4.4 million.

Condominiums

Condominium sales in the Snyderville Basin slipped slightly, down 2% with 240 total closings, and the median price declined 8% to $965,000. Canyons Village remained the most active submarket, with 104 closings and a 4% rise in median price to $1.3 million. Sun Peak/Bear Hollow followed with 26 sales and an 8% increase in median price to $1.2 million. Kimball recorded 47 sales but saw a 12% drop in median price to $720,000, while Pinebrook had 30 closings and a modest 1% dip to $953,000. Jeremy Ranch registered 10 condominium sales at $1.2 million, down 4%, and Silver Creek South had 17 closings with a 15% decrease in median price to $870,000.

Neighborhood Highlights - Jordanelle

SINGLE-FAMILY Homes

Across the greater Jordanelle area, there were 96 total closings – a 12% increase over the prior twelve-month period – with the median price rising 17% to $4.2 million.

Mayflower-Jordanelle recorded 15 sales and a 17% median price increase to $4 million. Tuhaye posted a strong 26% jump in median price to $5.9 million on 25 closings, while Hideout logged 20 sales with a 21% rise to $2.7 million. Deer Mountain saw 7 closings and a 31% decline in median price to $1.7 million. Rounding out the area, South Jordanelle registered 29 sales and a 5% uptick in median price to $4.3 million.

Condominiums

Jordanelle’s condominium market remained active, fueled by ongoing construction and sales at new communities such as Jordanelle Ridge and Mayflower Lakeside. Overall, unit sales increased 12%, though pricing continued to vary by development.

• Mayflower Lakeside: $1.6 million

• Pioche Village: $496,000

• Residences at Grand Hyatt: $2.1 million

The overall median price in the Mayflower–Jordanelle area climbed 21% to $1.5 million on 74 total sales. Deer Mountain recorded 64 closings but saw its median price decline 15% to $933,000. South Jordanelle followed with 10 closings and a 6% dip to $1.1 million.

Deer Valley East Village stood out with 76 closings and a dramatic 254% surge in median price to $1.6 million, while Hideout posted 63 closings and a 33% increase in median price to $1.8 million.

Heber Valley I Market Overview

SINGLE-FAMILY Homes

Single-family home sales across the Heber Valley rose 9% with 351 total closings, accompanied by a 9% increase in median price to $1.1 million.

Midway recorded 94 closings and a 13% median price increase to $1.2 million. Red Ledges saw 47 sales, with median prices edging down 5% to $2.8 million. South Fields logged 12 closings and a 4% decline in median price to $734,000.

Heber proper had 61 sales with a 4% dip in median price to $735,000, while Heber East posted 34 closings and a 10% drop to $1.3 million. In contrast, Heber North saw 33 sales and a 4% increase to $855,000. Timber Lakes rounded out the area with 46 closings and a 7% rise in median price to $803,000.

Condominiums

The condominium market in Heber Valley remained active, with sales up 86% to 119 total closings, while the median price held steady at $550,000.

Midway registered 23 closings and an 8% increase in median price to $510,000. Red Ledges recorded 5 sales with an unchanged median price of $1.7 million. In Heber proper, 30 sales closed with a 1% decline to $475,000, while Heber North saw the most dramatic shift. Sales surged 263% to 58 closings, though the median price dipped 7% to $555,000.

This report has been created in cooperation with KW Park City Keller Williams Real Estate, with stats provided by Rick Klein and the Park City Multiple Listing Service Quarter 3 2025 Statistics Report.

Curious how Q3 trends affect your property or buying strategy?

We’re happy to walk you through it. Contact us today to explore market data, listings, and expert insight tailored to your real estate goals in Park City and the surrounding Wasatch Back.

Call Drew Via & Annett Blankenship

The Park City Investor Team

KW Park City – Keller Williams Real Estate

435.640.6966